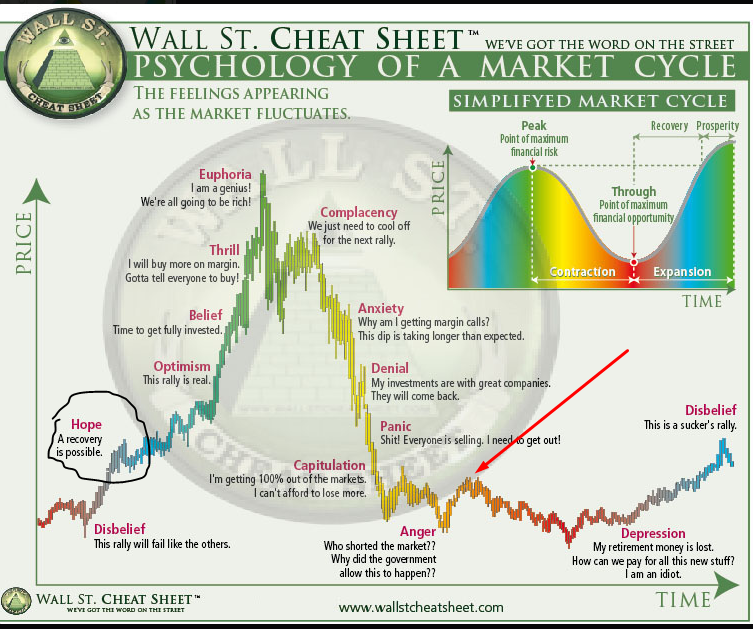

The FTX fiasco is nothing new for Bitcoin as it survived multiple exchange collapses, bear markets and even outright bans in its decade-plus existence.

The “Bitcoin-is-dead” gang is back and at it again. The fall of the FTX cryptocurrency exchange has resurrected these infamous critics that are once again blaming a robbery on the money that was stolen, and not the robber.

“We need regulation! Why did the government allow this to happen?” they scream.

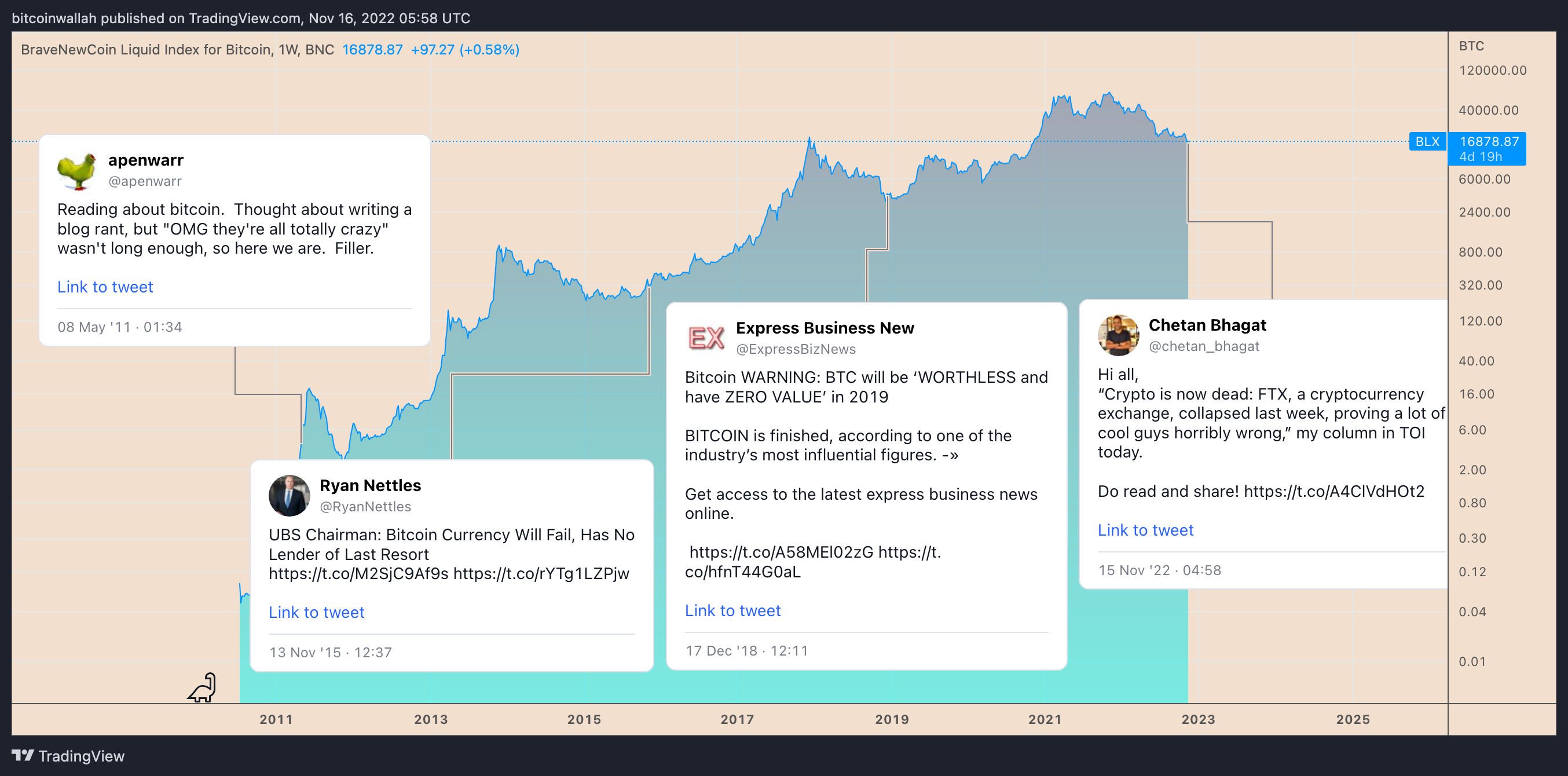

For instance, Chetan Bhagat, a renowned author from India, wrote a detailed “crypto” obituary, comparing the cryptocurrency sector to communism that promised decentralization but ended up with authoritarianism.

Perhaps unsurprisingly, his column conveniently used a melting Bitcoin (BTC) logo as its featured image.

Hi all,

“Crypto is now dead: FTX, a cryptocurrency exchange, collapsed last week, proving a lot of cool guys horribly wrong,” my column in TOI today.Do read and share! pic.twitter.com/A4ClVdHOt2

— Chetan Bhagat (@chetan_bhagat) November 15, 2022

Bhagat should have picked a more accurate image for his op-ed (melting FTX (FTT) Token?), particularly after looking at Bitcoin’s decade-plus history that has seen it surviving even nationwide bans. This includes 465 466 obituaries since its debut in 2009 when it traded for a few cents.

The FTX/Alameda’s collapse is similar to previous bearish trigger events like Mt. Gox in 2014. Therefore, this failure of centralization will once again underline what makes Bitcoin special, and why FTX is the opposite of Bitcoin and decentralization.

Moreover, the incident should also boost growth and development of in, non-custodial exchanges for Bitcoin that will help reduce dependency on trust.

FTX may have had zero Bitcoin in custody

Traders responded to FTX’s shocking collapse by pulling their BTC from custodial exchanges. Notably, the total amount of Bitcoin held by all exchanges dropped to 2.07 million BTC on Nov. 17 from 2.29 million BTC at the beginning of the month.

United States-based exchanges saw the biggest outflows, in particular, with users withdrawing over $1.5 billion in BTC in the past week alone.

On Nov. 9, FTX halted withdrawals of all cryptocurrencies, including Bitcoin, raising suspicions that the exchange did not have adequate reserves to meet the demand.

That was further evident in a leaked FTX balance sheet that showed the exchange having zero Bitcoin against its $1.4 billion liabilities in BTC. In other words, FTX enabled fractional-reserve Bitcoin trading.

“This is, on the one hand, bad for you as you will only find out if they have been swimming naked once the exchange implodes, accompanied by you losing all your funds,” Jan Wüstenfeld, writes independent market analyst. He adds:

“On the other hand, this artificially increases the bitcoin supply in the short-run, suppressing the price and preventing actual price discovery […] Yes, I know these are not real bitcoin, but as long as the exchanges issuing fake paper, Bitcoin remains operational, the effect is there.”

Thus, FTX’s little-to-negligible exposure to Bitcoin potentially reduces Its likelihood of selling any remaining funds to raise liquidity.

The incident is also likely to produce a new cohort of Bitcoin hodlers by forcing people to not keep their funds on risky exchanges and practice self-custody. While a decreasing amount of BTC on exchanges means fewer coins available to sell.

Sam Bankman-Fried was anti-Bitcoin

FTX founder Sam Bankman-Fried (SBF) was the Democrats’ second biggest donor after George Soros for the midterm elections, giving nearly $45 million to lobby for crypto regulations that would allegedly benefit his firm.

Related: US crypto exchanges lead Bitcoin exodus: Over $1.5B in BTC withdrawn in one week

But speculations are large that SBF attempted to tarnish Bitcoin’s growth through the U.S. lawmakers, as well as news articles, where he downplayed Bitcoin as an efficient payment system.

MSM lionized this shady character. For example, here are 2 of the 219 articles about him on @FT. @SBF_FTX’s anti-Bitcoin, pro-centralisation and pro-heavy-handed regulation values certainly aligned with theirs.

Was he the poster boy for an orchestrated propaganda campaign? https://t.co/urJcu6mqB6 pic.twitter.com/PTIn1JudXG

— Bitcoms (@bitcoms) November 15, 2022

Other commentators have also pointed out a connection between SBF and anti-crypto U.S. Senator Elizabeth Warren, noting the former’s father, Joseph Bankman, helped the politician draft tax legislation in 2016.

This is crazy:

Elizabeth Warren is known for being the anti-crypto Senator

Who helped her draft her tax legislation in 2016?

None other than Joseph (Joe) Bankman, the father of SBFhttps://t.co/QMYkC2gpE9

— Ryan Shea (@ryaneshea) November 15, 2022

SBF’s influence among U.S. lawmakers is now gone with him facing potential criminal charges for illegally using customer funds for FTX trades.

Press “F” to flush

Past cryptocurrency market downturns have roots in the failure of centralized players as well as “altcoins” that ultimately ended up being a money-grab.

FTX’s token FTT is just the latest example. Other failed projects that triggered a market downturn just this year include the Defi lending platform Celsius Network (CEL) and Terra (LUNA).

FTX is the opposite of #Bitcoin #Bitcoin ’s protocol was created precisely to prevent Ponzi schemes, bank runs, Enron’s, WorldCom’s, Bernie Madoff’s, Sam Bankman-Fried’s…

…bailouts and wealth reassignments.

Some understand it, some not yet.

We’re still early.

/21m

— Nayib Bukele (@nayibbukele) November 14, 2022

Created and operated by centralized entities, the supply of these tokens, and therefore price, becomes vulnerable to manipulation: undisclosed pre-mine allocations, insider VC deals, small float vs. total supply, you name it.

It is exposure to such (crap) tokens, particularly in the form of collateral, that ultimately drove crypto hedge funds Three Arrow Capital, FTX’s sister firm Alameda Research, and many others to the ground.

“In our view, the bubble in crypto that popped this year was in the atmosphere of tokens being created just for speculative purposes,” noted BOOX Research, adding:

“While we can debate which cryptos are ‘bad money driving out the good’, FTT and LUNA are just two examples everyone can agree should not have existed.”

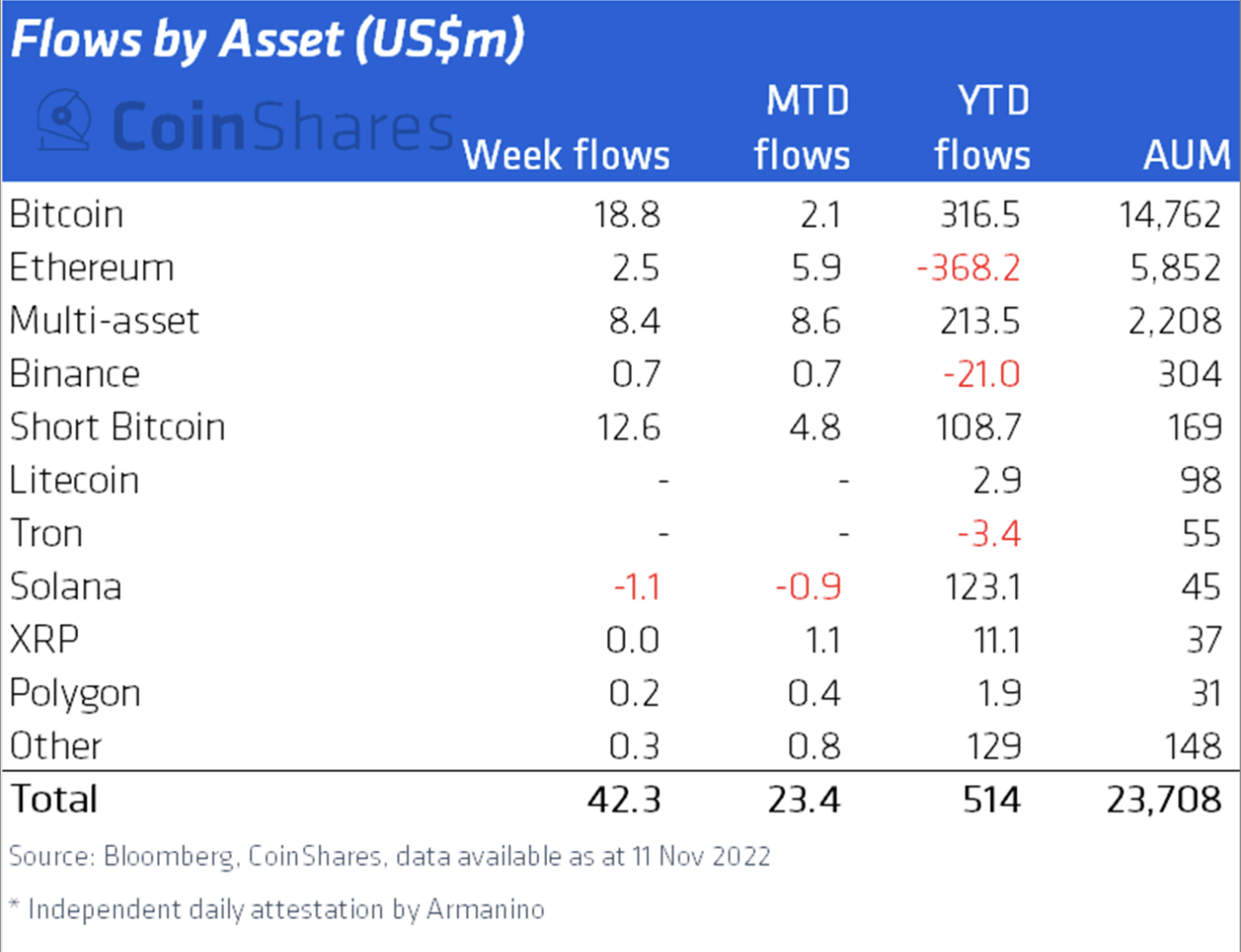

Therefore, a market flush of altcoins that should not have ever existed, FTT included, may further strengthen investors’ trust in Bitcoin. Early data is showing the same, with CoinShares reporting an inflow uptick into Bitcoin-based investment funds.

Notably, Bitcoin-based investment vehicles attracted $18.8 million to their coffers in the week ending Nov. 11, bringing its year-to-date inflows to $316.50 million.

“The inflows began later in the week on the back of extreme price weakness prompted by the FTX/Alameda collapse,” noted James Butterfill, head of research at CoinShares, adding:

“It suggests that investors see this price weakness as an opportunity, differentiating between ‘trusted’ third parties and an inherently trustless system.”

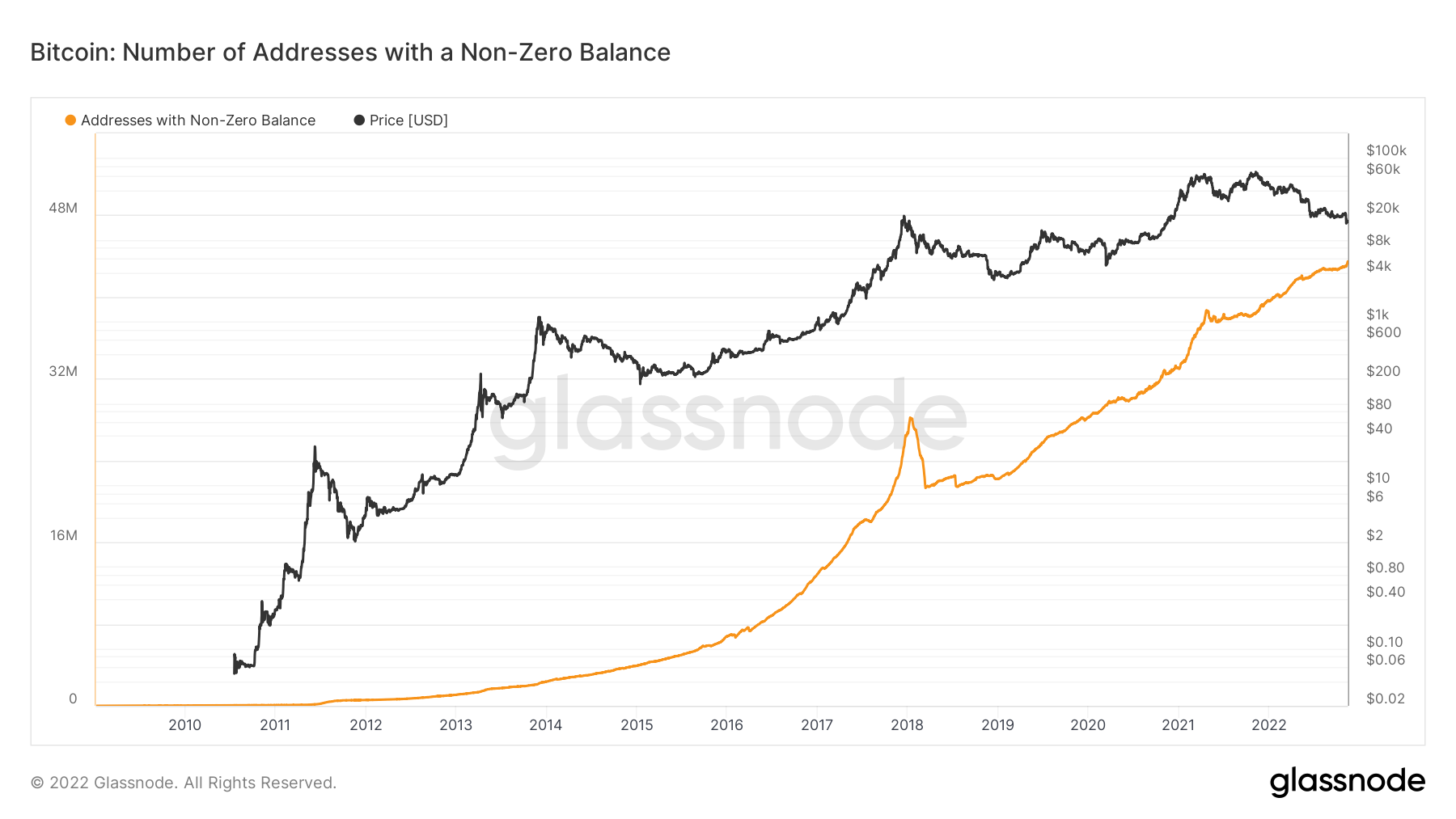

Meanwhile, Bitcoin is not witnessing a collapse in demand in the current bear market compared to 2018, on-chain data reveals.

The number of non-zero Bitcoin addresses has continued to climb despite the price downtrend, hitting a record high of 43.14 million as of Nov. 16.

In comparison, the 2018 bear market saw a substantial drop in the number of non-zero Bitcoin addresses, suggesting traders have become relatively more confident about a price recovery, especially as the FTX domino effect clears out the dead wood.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.