It’s not expected to come into force until 2025, but new publications from the FCA and BOE shed light on regulators’ thinking.

A suite of documents was published in the United Kingdom on Nov. 6 that concern stablecoin regulation. The Financial Conduct Authority (FCA) released a discussion paper, as did the Bank of England (BOE). To accompany those, the BOE’s Prudential Regulatory Authority (PRA) released a letter to CEOs of deposit-taking institutions, and the BOE released a “cross-authority roadmap” to link them together.

His Majesty’s Treasury set the stage for the flurry of releases on Oct. 30 with a short document previewing plans for regulation. The FCA paper explored the same ground in much greater detail.

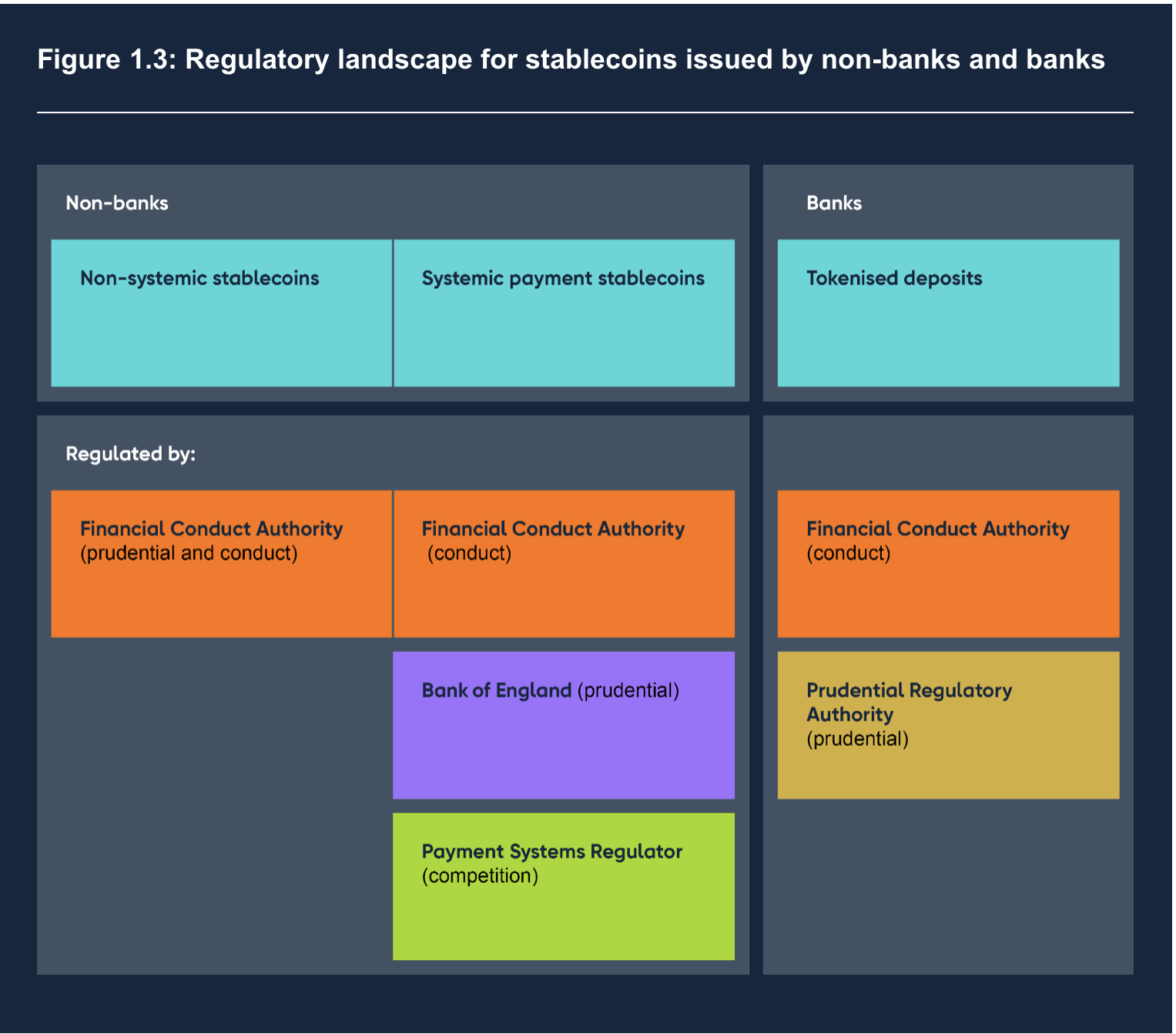

Stablecoin regulation is the first step to broader crypto-asset regulation, the FCA said. The discussion paper outlined potential retail and wholesale stablecoin use cases. Its discussion included auditing and reporting, the backing of coins owned by the issuer and the independence of the backing assets’ custodian.

The paper concentrated on ways in which the principle of “same risk, same regulator outcome” could be applied. It proposed using the existing client assets regime as the basis of rules on redemption and custodianship and the senior management arrangements, systems and controls sourcebook to organize business affairs. There are existing operational resilience and financial crime frameworks, as well as numerous others.

The UK FCA is proposing that stablecoin holders have the right of direct redemption. Which makes issuers a lot more like banks and will raise a bunch of AML/KYC issues for issuers pic.twitter.com/lZLQXlmemu

— Sean Tuffy (@SMTuffy) November 6, 2023

The FCA is considering adapting existing prudential requirements for regulated stablecoin issuers and custodians from the existing regime and making them applicable to other crypto assets eventually.

The BOE paper looked at the use of sterling-based retail-focused stablecoin in systemic payment systems. It considered transfer function and requirements for wallet providers and other services, and it partially overlapped with the FCA’s discussion of stablecoin issuers and deposit protection.

Related: UK crypto businesses to comply with FATF Travel Rule beginning in September

The BOE will “rely on” the FCA to regulate custodians, it said, but it left open the possibility of imposing requirements of its own, if necessary. It pointed to Anti-Money Laundering and Know Your Customer requirements for unhosted wallets and off-chain transactions as potential regulatory sore points.

The BOE PRA letter emphasized that the difference between “e-money or regulated stablecoins” and other types of deposits have to be clearly maintained:

“With the emergence of multiple forms of digital money and money-like instruments, there is a risk of confusion among customers, especially retail customers, if deposit- taking entities were to offer e-money or regulated stablecoins under the same branding as their deposits.”

Deposit-taking institutions should limit their innovation to deposits. Issuance activities should have distinct branding, the PRA advised. An issuer that wants to take deposits as well should move quickly and involve the PRA in the process. Finally, innovations in deposit-taking are also subject to rules and requirements, it reminded.

The BOE roadmap included a timeline, with an implementation date of 2025.

Magazine: Unstablecoins: Depegging, bank runs and other risks loom